Cash flow reporting shapes how CFOs and finance leaders communicate their company’s financial health to stakeholders, lenders, and boards. Yet one of the most consequential choices in that process, the direct vs indirect cash flow method, often gets decided by default rather than by strategy. Both methods produce the same bottom-line number on your cash flow statement, but they get there through fundamentally different paths, and each one tells a different story about where your cash actually comes from and where it goes.

The direct method itemizes actual cash receipts and payments. The indirect method starts with net income and adjusts for non-cash items. Choosing the right one affects reporting clarity, audit readiness, and the quality of insight your leadership team gets from the numbers. For midsized companies running NetSuite or Acumatica, this choice also determines how much of your cash flow reporting can be automated within your ERP, something we help clients configure and optimize every day at Concentrus.

This article breaks down both methods side by side, definitions, formulas, pros, cons, and worked examples, so you can determine which approach fits your organization. Whether you’re implementing a new ERP system or rescuing an underperforming one, understanding these methods is essential to building financial reports that actually drive decisions.

What the Direct and Indirect Methods Show

Both methods apply specifically to the operating activities section of your cash flow statement. The financing and investing sections look identical regardless of which approach you use. That means the choice between the direct vs indirect cash flow method affects only one part of your statement, but it’s the part that matters most for understanding how your core business operations actually generate or consume cash during a given period.

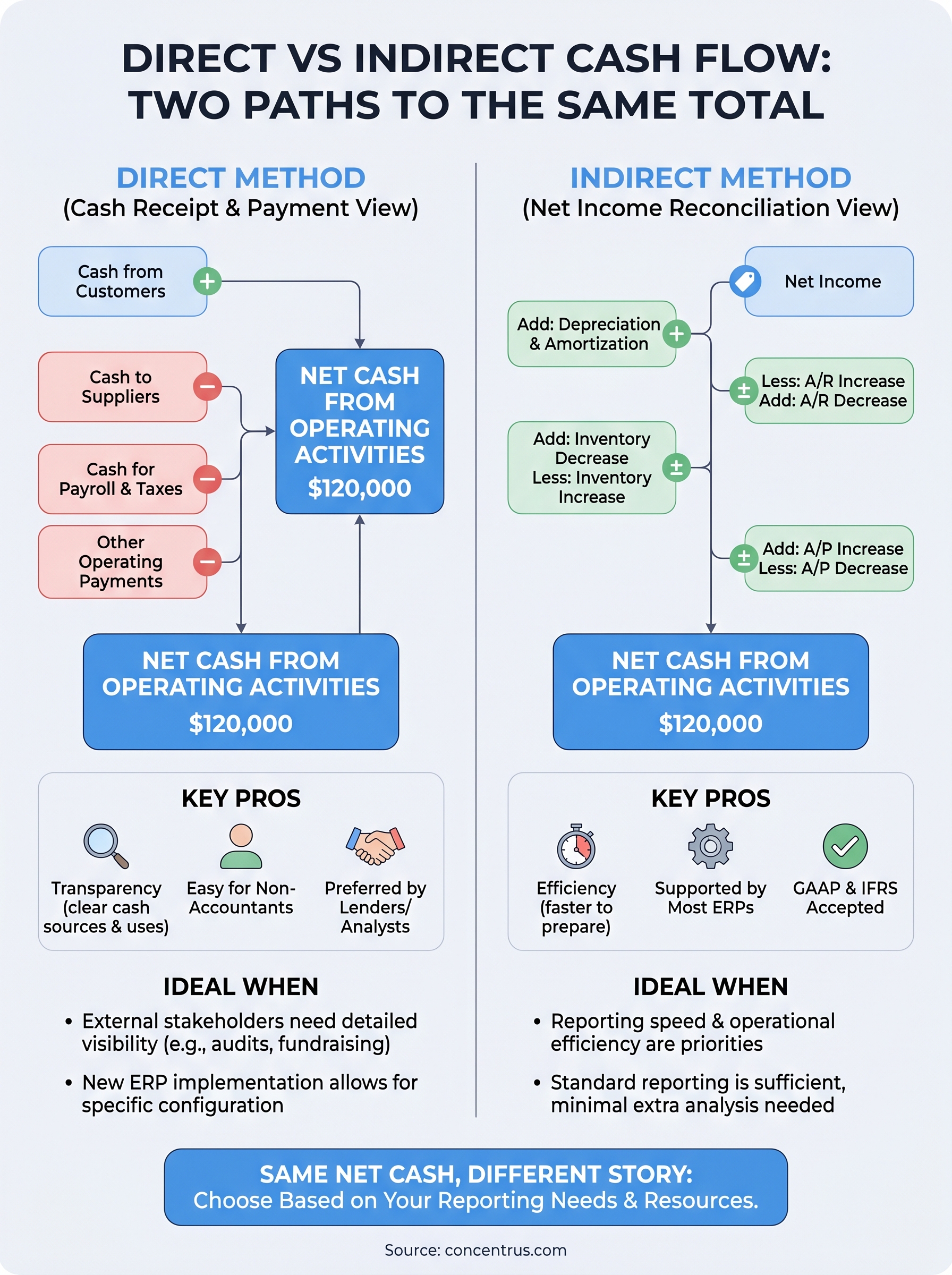

The direct method: cash in and cash out by source

The direct method lists every significant category of cash receipt and cash payment from operating activities. Instead of adjusting net income, it tracks real money movement: what customers actually paid you, what you actually paid suppliers, what went out for payroll and taxes, and what came in from other operating sources. The result is a granular view of operating cash flow that mirrors how cash physically moved through your business.

Producing this report requires your accounting team to separately identify and categorize each cash transaction from operations rather than deriving cash figures from accrual-based income statement data. Most companies don’t record transactions this way by default in their general ledger, which is precisely why ERP configuration matters. Systems like NetSuite and Acumatica can be structured to capture the data fields needed for a direct method statement, but it takes deliberate setup, clean chart-of-accounts design, and ongoing discipline to maintain that level of detail accurately.

The direct method gives lenders, investors, and board members a transaction-level picture of where operating cash originates, which is far more transparent than a series of reconciling adjustments layered on top of net income.

The indirect method: from net income to cash

The indirect method starts with your net income figure from the income statement and works backward to reconcile it to actual operating cash flow. It adds back non-cash charges like depreciation and amortization, then adjusts for changes in working capital accounts: accounts receivable, inventory, accounts payable, and accrued liabilities. The final number is your net cash provided by operating activities.

This approach works because accrual accounting records revenue when it’s earned and expenses when they’re incurred, not when cash actually changes hands. The indirect method strips out those timing differences systematically to show the cash reality behind your income number. For most midsized companies, this is the method their accounting systems already support by default, since it draws directly from income statement and balance sheet data that’s already being captured through normal month-end close processes.

Why both methods reach the same number

Despite their different starting points and structures, both methods produce the identical net cash from operating activities when prepared correctly. The direct method counts actual cash receipts and payments; the indirect method adjusts accrual-based income until it reconciles to that same cash figure. They are two different paths to the same result.

This equivalency matters because it confirms that your choice of method is a reporting and presentation decision, not an accounting or financial one. It has no impact on your actual cash balance, your tax obligations, or your financial position. What it does shape is how easily your stakeholders can understand the operating section of your cash flow statement and how efficiently your finance team can generate that statement every reporting cycle.

Pros and Cons of Each Method

The right method for your organization depends on what you need from your financial reporting and how your accounting systems are configured. Understanding the strengths and limitations of each approach helps you make a deliberate choice rather than defaulting to whatever your ERP produces out of the box.

Direct method: transparency at a cost

The direct method gives stakeholders the clearest possible view of operating cash flows. Lenders, investors, and board members can see exactly what customers paid you and what you paid out across each operating category without working through a set of reconciling adjustments. Both the FASB and IASB have historically encouraged its use for this reason, and FASB standards note the direct method as the preferred presentation approach.

Transparency comes with a real operational cost: producing a direct method statement requires tracking cash transactions at a level of detail most general ledgers don’t capture by default.

- Pros: granular view of cash sources and uses, easier for non-accountants to interpret, preferred by many lenders and analysts

- Cons: significantly more time-intensive to prepare, requires specific ERP configuration, most companies don’t maintain records at this level without deliberate setup

Indirect method: efficiency with trade-offs

The indirect method is the dominant choice for midsized companies precisely because it draws directly from data your accounting team already generates through normal close processes. Your income statement and balance sheet changes provide everything needed, so there’s no requirement to separately track individual cash receipts or disbursements.

Comparing the direct vs indirect cash flow method on efficiency, the indirect approach wins decisively for most organizations. Finance teams can produce it faster, ERP systems like NetSuite and Acumatica generate it with minimal additional configuration, and it satisfies both GAAP and IFRS reporting requirements. The downside is that working capital adjustments and non-cash addbacks can obscure the actual cash mechanics of your business from readers who aren’t financially sophisticated.

- Pros: faster to prepare, supported natively by most ERP systems, widely accepted under GAAP and IFRS

- Cons: less intuitive for non-finance stakeholders, buries operating cash drivers inside reconciling adjustments, requires additional analysis to identify what’s actually driving cash generation

Step-by-Step: Build Each Method with Examples

Working through a concrete example clarifies the direct vs indirect cash flow method far more effectively than comparing definitions alone. The scenario below uses the same fictional midsized company for both methods, so you can see exactly how each approach handles the same underlying financial data and arrives at the same operating cash total.

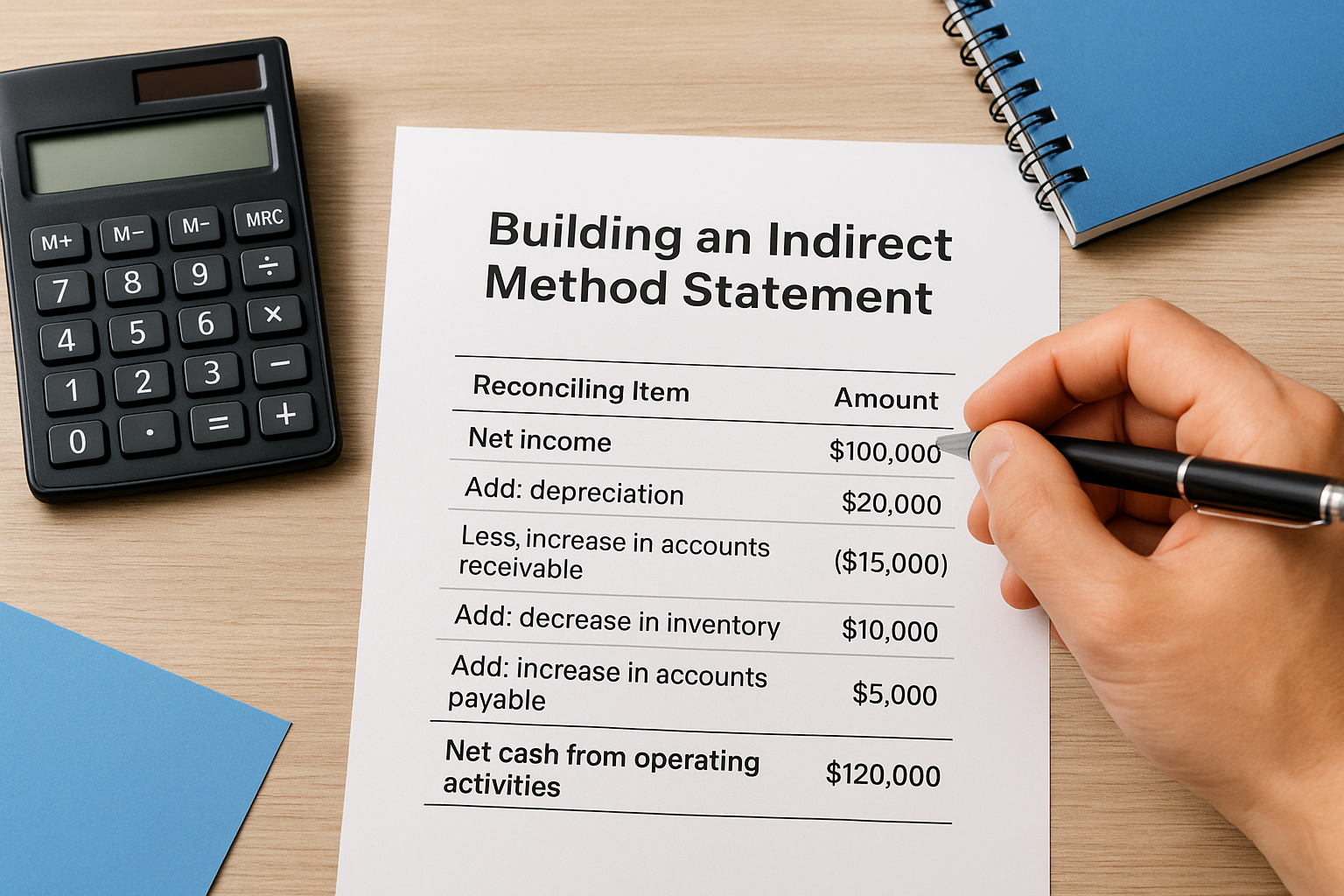

Assume your company reports $100,000 in net income for the quarter, has $20,000 in depreciation, and carries working capital changes that include a $15,000 increase in accounts receivable, a $10,000 decrease in inventory, and a $5,000 increase in accounts payable.

Building a Direct Method Statement

The direct method requires you to identify each category of cash receipt and payment from actual transactions rather than deriving them from income statement accounts. For this example, your team pulls transaction-level data to produce the following:

| Operating Cash Activity | Amount |

|---|---|

| Cash received from customers | $500,000 |

| Cash paid to suppliers | ($200,000) |

| Cash paid for salaries | ($150,000) |

| Cash paid for taxes | ($30,000) |

| Net cash from operating activities | $120,000 |

Each line represents real cash movement during the period. Your accounting system must be configured to capture receipts and disbursements at this level of detail, which is why ERP setup decisions directly affect whether your team can produce this statement efficiently.

Building an Indirect Method Statement

The indirect method starts with the net income figure already sitting on your income statement and reconciles it to operating cash through a series of adjustments. Using the same company data:

| Reconciling Item | Amount |

|---|---|

| Net income | $100,000 |

| Add: depreciation | $20,000 |

| Less: increase in accounts receivable | ($15,000) |

| Add: decrease in inventory | $10,000 |

| Add: increase in accounts payable | $5,000 |

| Net cash from operating activities | $120,000 |

Both methods produce $120,000, confirming that your method choice affects presentation only, not the actual cash your business generated.

Your ERP system can generate the indirect version automatically once your balance sheet and income statement accounts are properly mapped, which is why most midsized companies default to this approach when they go live on NetSuite or Acumatica.

Formulas and Common Adjustments Explained

Understanding the math behind each method helps you validate the numbers your ERP generates and catch errors before they reach your board or lenders. Both methods follow a defined structure, and knowing the core formula for each one gives your finance team a reliable framework to work from, whether you’re building the statement manually or reviewing system-generated output.

The Direct Method Formula

The direct method formula is straightforward: you sum all cash inflows from operating activities and subtract all cash outflows from operating activities to arrive at net cash from operations.

Direct Method Formula:

Net Cash from Operating Activities = Cash Received from Customers – Cash Paid to Suppliers – Cash Paid for Salaries – Cash Paid for Taxes – Other Operating Cash Payments

Each input requires your accounting system to capture actual cash movement rather than accrual-based figures. If your ERP isn’t configured to tag transactions by operating cash category, your team will spend significant time manually reconstructing these numbers at every period close.

The Indirect Method Formula and Key Adjustments

The indirect method formula starts with net income and applies a series of structured adjustments to convert your accrual-based income figure into actual operating cash flow. When you compare the direct vs indirect cash flow method at the formula level, the indirect approach involves more moving parts, but each adjustment follows a consistent logic.

Indirect Method Formula:

Net Cash from Operating Activities = Net Income + Non-Cash Charges + Changes in Working Capital

Getting the working capital adjustments right is where most errors occur, so building these reconciliation steps directly into your ERP close checklist saves time and prevents misstatements.

The most common adjustments include:

- Depreciation and amortization: Added back because they reduce net income but involve no cash outflow

- Accounts receivable increase: Subtracted because revenue was recorded but cash hasn’t been collected yet

- Accounts receivable decrease: Added because cash was collected from prior-period revenue

- Inventory decrease: Added because goods sold weren’t replaced with new cash purchases

- Accounts payable increase: Added because expenses were recorded but cash hasn’t left yet

- Accounts payable decrease: Subtracted because cash paid exceeded the current period expense

Each adjustment corrects for the timing gap between when your income statement recognizes an item and when cash actually moves.

How to Choose the Right Method for Your Business

Choosing between the direct vs indirect cash flow method is not a universal decision. The right answer depends on your reporting obligations, stakeholder expectations, and how your accounting systems are currently configured. Before defaulting to whatever your ERP produces out of the box, evaluate a few specific factors that point clearly toward one method or the other.

When the direct method makes sense

The direct method fits your organization best when external stakeholders require detailed cash visibility and your finance team has the capacity to support the additional data capture it demands. Lenders evaluating credit facilities, private equity partners reviewing operational performance, and boards focused on cash generation all benefit from seeing explicit receipts and payments broken out by category rather than a reconciliation of net income.

If you’re preparing for a debt raise, an acquisition, or a strategic audit, the direct method gives your reviewers the clearest picture of how your operations generate cash.

You should also consider the direct method when your ERP implementation is still in progress and you have the opportunity to configure your chart of accounts and transaction tagging before go-live. Retrofitting an existing system to support direct method reporting is significantly harder than building it in from the start.

When the indirect method fits better

The indirect method is the practical choice for most midsized companies operating under GAAP, particularly when your team is already producing accurate income statements and balance sheets through a disciplined close process. Your ERP system, whether NetSuite or Acumatica, can generate the indirect method statement with minimal manual effort because it draws entirely from data your team already maintains.

You should lean toward the indirect method when reporting speed and operational efficiency outweigh the need for granular cash transparency. Most audit firms, tax advisors, and institutional lenders accept the indirect method without question, and it satisfies both GAAP and IFRS requirements without additional configuration overhead.

The practical decision framework

Evaluate three factors: who reads your cash flow statement, what your current ERP produces by default, and whether your finance team has bandwidth to maintain transaction-level cash records. If all three point toward simplicity, choose indirect. If stakeholder transparency is a priority and your systems support the configuration, invest in direct.

Key Takeaways for Finance Leaders

The direct vs indirect cash flow method decision comes down to two priorities: transparency and efficiency. The direct method gives stakeholders a clear view of real cash movements by category, while the indirect method converts net income into operating cash through structured adjustments, drawing from data your team already produces.

For most midsized companies, the indirect method fits standard operations without additional ERP configuration. The direct method earns its place when lenders, investors, or boards need granular cash visibility, especially during audits, fundraising rounds, or strategic reviews. Either way, your ERP configuration determines how much of this work gets automated versus handled manually each close cycle.

Your cash flow reporting should give your leadership team clear, reliable insight without consuming your finance team’s time. If your current ERP isn’t delivering that, connect with an ERP and ROI specialist at Concentrus to build reporting that drives real decisions.