Choosing between a perpetual vs periodic inventory system directly impacts your financial reporting accuracy, operational efficiency, and ability to make informed decisions. For CFOs at midsized companies, this choice isn’t just an accounting preference, it’s a strategic decision that affects cash flow visibility and profitability tracking.

The perpetual system updates inventory records in real time with every transaction, while the periodic system calculates inventory only at specific intervals. Each approach carries distinct implications for your cost of goods sold calculations, journal entries, and overall financial control. Understanding these differences helps you align your inventory management with your company’s growth trajectory and reporting requirements.

At Concentrus, we implement NetSuite and Acumatica ERP systems designed to support either inventory method, or help you transition between them. Our focus on measurable ROI means your inventory system should work for your financial goals, not against them. This guide breaks down the key differences between perpetual and periodic inventory systems, their accounting treatments, and the practical advantages and disadvantages of each, so you can determine which approach fits your business.

Perpetual vs periodic inventory system basics

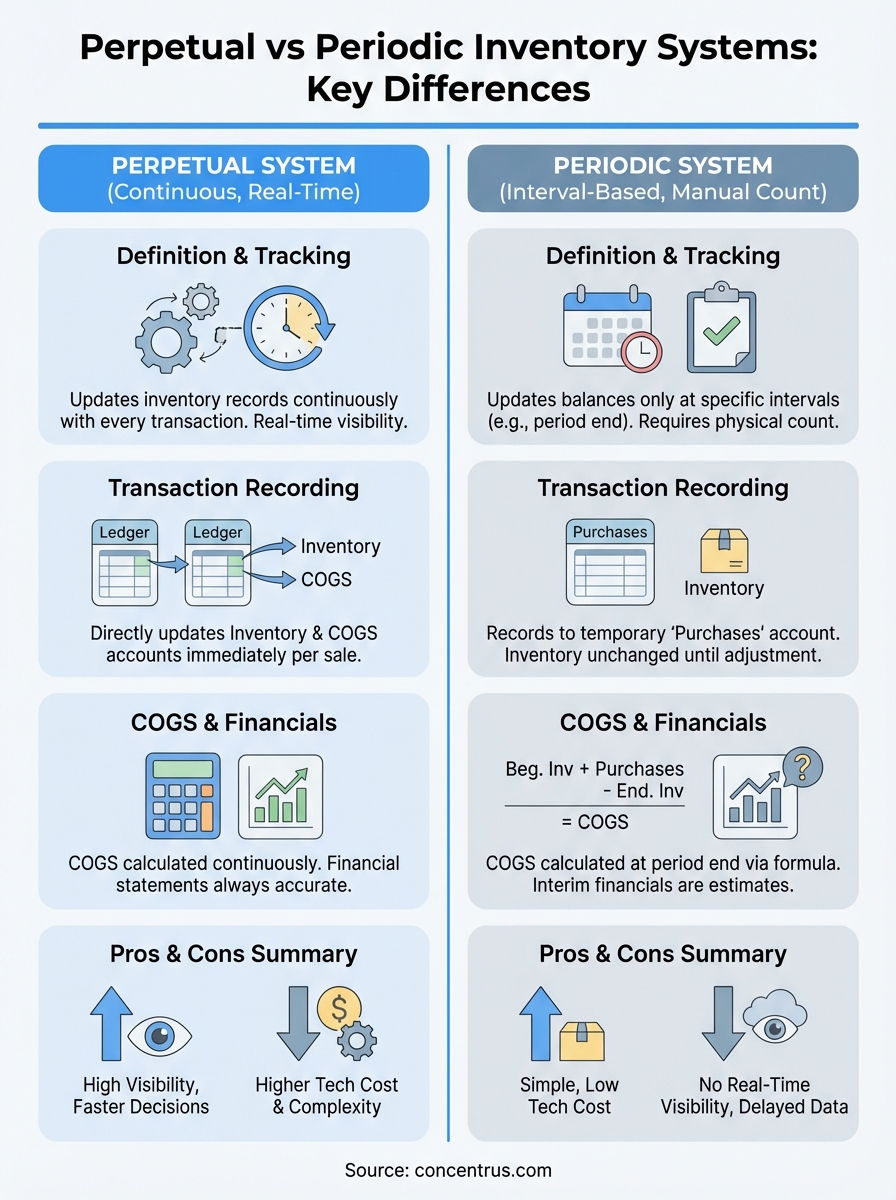

The fundamental difference between a perpetual vs periodic inventory system lies in when and how you track your inventory balances. A perpetual system maintains continuous, real-time records of every inventory transaction as it happens, while a periodic system updates inventory balances only at specific intervals, typically at the end of each accounting period. Your choice between these methods determines how quickly you can access accurate inventory data and how much manual effort your team invests in tracking stock levels.

What defines a perpetual inventory system

A perpetual inventory system automatically updates your inventory records with every purchase, sale, or adjustment the moment the transaction occurs. Your ERP software captures each movement instantly, adjusting quantities and values in your general ledger without waiting for a physical count. This system requires integrated technology like barcode scanners, point-of-sale systems, or warehouse management tools that communicate directly with your accounting platform.

Your inventory account increases when you receive goods and decreases when you make sales, with the cost of goods sold calculated transaction by transaction. This means you always know your theoretical inventory balance at any given moment. The system tracks not just quantities but also the specific cost layers of your inventory, making methods like FIFO (first in, first out) or weighted average automatic and precise.

Perpetual inventory gives you real-time visibility into stock levels, enabling faster decision-making and more accurate financial reporting throughout the accounting period.

What defines a periodic inventory system

A periodic inventory system records purchases in a separate purchases account rather than directly updating your inventory balance. You don’t adjust your inventory account for individual transactions throughout the period. Instead, you determine your ending inventory by conducting a physical count at period end, typically monthly, quarterly, or annually.

When you perform the physical count, you calculate cost of goods sold using the formula: beginning inventory plus purchases minus ending inventory. Your inventory account stays static between counts, showing the same balance from one period close to the next. This approach requires less sophisticated technology and fewer real-time integrations, making it simpler to implement but less informative for day-to-day operations.

The periodic method works well for businesses with relatively stable inventory, lower transaction volumes, or simple product lines. However, you sacrifice the ability to detect shrinkage, theft, or recording errors until you complete your next physical count. Your financial statements between counting periods reflect estimates rather than actual inventory positions, which can limit your ability to respond quickly to stock issues or demand changes.

How each system records transactions

The way you record inventory transactions differs significantly between a perpetual vs periodic inventory system, affecting both your accounting entries and your real-time visibility into stock levels. Each system follows distinct rules for documenting purchases, sales, and returns, which directly impacts your financial statement accuracy and operational control. Understanding these recording differences helps you anticipate the workload and technical requirements each method demands.

Transaction recording in perpetual systems

When you purchase inventory under a perpetual system, you debit your inventory account directly and credit either cash or accounts payable. Each sale triggers two simultaneous journal entries: one to record the revenue (debit cash or accounts receivable, credit sales) and another to record the cost (debit cost of goods sold, credit inventory). Your inventory account decreases immediately, and your COGS account increases with every transaction.

Your ERP system calculates the cost to remove from inventory automatically based on your chosen cost flow assumption (FIFO, LIFO, or weighted average). If you receive a purchase return, you credit inventory and debit accounts payable. For sales returns, you reverse both the revenue entry and the COGS entry, putting the inventory back on your books at its original cost. This continuous updating means your general ledger always reflects your most recent inventory position.

Perpetual systems create a detailed transaction trail that lets you trace every inventory movement from purchase through sale to your financial statements.

Transaction recording in periodic systems

Your periodic system handles purchases differently by debiting a temporary purchases account rather than directly updating inventory. You record the purchase transaction with a debit to purchases and a credit to cash or accounts payable, leaving your inventory account untouched. When you make sales, you only record the revenue side of the transaction (debit accounts receivable, credit sales) without adjusting inventory or recording COGS at the transaction level.

At period end, you calculate COGS through a closing entry process. You transfer the beginning inventory balance, all purchases, and purchase-related accounts into COGS, then subtract your ending inventory value (determined by physical count) to arrive at the cost of goods sold for the period. This closing process resets your inventory account to the new ending balance and zeros out your purchases account, preparing your books for the next accounting period.

How COGS and financials differ

Your choice between a perpetual vs periodic inventory system fundamentally changes how you calculate cost of goods sold and when that information appears on your financial statements. These timing differences affect your profit margins, inventory valuations, and the reliability of your interim financial reports. Understanding these distinctions helps you anticipate the financial reporting capabilities each system offers throughout your accounting periods.

COGS calculation timing and accuracy

Perpetual systems calculate your COGS with every single sale transaction, giving you up-to-the-minute accuracy on your gross profit margins. Your ERP automatically applies your cost flow method to determine the exact cost of each item sold, then immediately records that expense. This means you can pull a profit and loss statement at any moment and see accurate COGS figures without waiting for period end or conducting physical counts.

Periodic systems calculate COGS only after you complete your physical inventory count at period end. You arrive at this figure through the formula: beginning inventory plus purchases minus ending inventory equals cost of goods sold. Your COGS remains unknown during the accounting period, making your interim financial statements less reliable. Any errors in your physical count directly impact your COGS calculation, potentially overstating or understating your profitability for that entire period.

Perpetual systems give you continuous COGS visibility that enables faster financial decision-making and more accurate interim reporting compared to waiting for periodic counts.

Financial statement implications

Your balance sheet under a perpetual system shows real-time inventory values that change with every transaction, reflecting your theoretical stock position at any reporting date. The income statement displays COGS that matches actual sales activity, providing reliable gross profit calculations throughout the year. This continuous updating supports more frequent financial closes and gives stakeholders current information for strategic decisions.

Periodic systems keep your inventory account static between physical counts, showing the same balance regardless of purchases or sales activity. Your income statement can’t show accurate COGS until you complete the count and closing entries. This delay means your gross profit figures during the period are estimates at best, limiting your ability to respond quickly to margin pressure or pricing opportunities.

Pros, cons, and risk factors

Evaluating the advantages and disadvantages of a perpetual vs periodic inventory system requires you to weigh real-time accuracy against implementation complexity and cost. Each approach carries specific benefits and limitations that affect your operational efficiency, financial reporting quality, and resource requirements. Understanding these trade-offs helps you anticipate the full impact of your inventory method choice on your finance team’s workload and your company’s decision-making capabilities.

Perpetual system advantages and disadvantages

Perpetual systems give you immediate visibility into stock levels, enabling faster responses to shortages, theft, or demand spikes. Your finance team can close books more quickly because COGS calculates automatically, and you can generate accurate financial statements at any time without waiting for physical counts. This real-time data supports better inventory planning, reduces stockouts, and helps you identify slow-moving products before they become write-off problems.

The disadvantages center on higher upfront costs and technical complexity. You need integrated ERP software, barcode scanners, and trained staff to maintain the system properly. Implementation requires more time and resources than periodic methods, and ongoing maintenance demands continuous attention to data quality. System errors or incorrect entries immediately affect your financials, making data accuracy discipline critical for success.

Periodic system advantages and disadvantages

Periodic systems require minimal technology investment and simpler staff training, making them accessible for smaller operations or businesses with limited IT resources. Your accounting team handles fewer real-time entries, and you avoid the complexity of maintaining integrated inventory management software. This approach works well when you carry relatively few SKUs or have stable, predictable inventory movement that doesn’t require constant monitoring.

However, you sacrifice visibility between counting periods, making it impossible to detect theft, spoilage, or recording errors until your next physical count. Your interim financial statements lack accurate COGS figures, limiting your ability to make timely pricing or purchasing decisions. The manual counting process consumes significant labor hours and introduces human error risk that can distort your profitability reporting.

Periodic systems trade lower technology costs for reduced visibility and delayed financial information that can handicap strategic decision-making.

Risk factors to consider

Both systems carry specific risks you need to manage actively. Perpetual systems face data integrity risks when staff bypass proper procedures or when system integrations fail, creating discrepancies between physical inventory and recorded balances. Periodic systems expose you to extended periods of uncertainty where you operate without knowing your true inventory position, increasing the risk of stockouts or overstock situations that tie up working capital unnecessarily.

How to choose and implement the right system

Your decision between a perpetual vs periodic inventory system should align with your transaction volume, product complexity, and financial reporting needs. Start by evaluating your current inventory turnover rates, the number of SKUs you manage, and how frequently your stakeholders need accurate inventory data for decision-making. Companies processing hundreds of transactions daily or managing multiple warehouse locations typically benefit more from perpetual systems, while businesses with simpler operations and lower volumes may find periodic methods sufficient.

Assess your business requirements

Examine your existing technology infrastructure and your team’s technical capabilities before committing to either system. Perpetual systems demand integrated ERP platforms, reliable network connectivity, and staff trained in real-time data entry procedures. Calculate the total cost of ownership including software licenses, hardware investments, training expenses, and ongoing maintenance requirements to understand your true implementation burden.

Consider your industry’s compliance requirements and how quickly you need to detect inventory discrepancies. Regulated industries or businesses with high-value inventory often require the audit trail and real-time visibility that perpetual systems provide. Your growth plans matter too, since scaling a periodic system becomes increasingly difficult as transaction volumes rise and product lines expand.

Plan your implementation approach

Begin your perpetual system implementation by mapping all inventory touchpoints where transactions occur, from receiving docks to sales counters. Identify the integration points between your inventory management system and accounting platform, ensuring data flows seamlessly without manual intervention. Test your processes with a pilot program on limited SKUs before rolling out company-wide to catch configuration issues early.

Successful implementation requires thorough staff training on transaction recording procedures and regular reconciliation between physical counts and system records to maintain data integrity.

Build regular cycle counting into your perpetual system routine to verify system accuracy without disrupting operations. For periodic systems, establish clear counting schedules and documentation procedures that minimize business interruption while ensuring accurate physical inventory verification.

Key takeaways

Your choice between a perpetual vs periodic inventory system shapes your financial reporting accuracy, operational visibility, and resource requirements. Perpetual systems deliver real-time inventory tracking and continuous COGS calculations that support faster decision-making and more reliable interim financial statements, though they require greater technology investment and staff training. Periodic systems offer simpler implementation and lower costs but sacrifice visibility between counting periods and delay your COGS calculations until you complete physical inventories.

The right system aligns with your transaction volume, product complexity, and growth trajectory. Higher volumes and multiple locations typically justify perpetual systems, while businesses with simpler operations may succeed with periodic methods. Whichever approach you choose, proper implementation and ongoing maintenance determine whether your inventory system supports or hinders your financial goals.

At Concentrus, we implement NetSuite and Acumatica ERP systems designed to support your chosen inventory method while delivering measurable ROI through our proprietary ROI Roadmap™ methodology. Your inventory management should drive profitability, not create reporting challenges that limit strategic visibility.